AI Software Stocks: What They Are and How to Evaluate Them in 2026

Investors keep asking me the same thing: which AI software stocks are worth owning, and which are just riding hype? The category has widened fast. Knowing what you actually own matters more now than it did a year ago.

AI software stocks are shares in companies whose revenue depends on artificial intelligence software, not just chips or hardware. The group spans model builders, enterprise platforms, and application vendors. In my coverage, the winners share one trait: real, recurring AI revenue.

What Counts as an AI Software Stock?

An AI software stock is a company that sells AI-driven software as its core product or as a fast-growing revenue line. This is different from AI hardware names like Nvidia, which sell the chips underneath.

The line gets blurry, so I use a simple test. Does AI software drive the revenue story, or is AI just a marketing label? If the company would post similar numbers without its AI products, it belongs in a different bucket.

Three layers make up the group:

Model and platform builders. Companies training and licensing large models, or renting them through the cloud. Microsoft, Alphabet, and Amazon lead here through their cloud arms and model partnerships.

Enterprise AI platforms. Firms selling AI tools that plug into business workflows. Palantir, ServiceNow, and Salesforce sit in this layer.

Application and vertical vendors. Smaller companies applying AI to one job, such as coding, customer service, or security.

Which AI Software Stocks Get the Most Attention in 2026?

The names investors track most in 2026 are Microsoft, Alphabet, Palantir, ServiceNow, Salesforce, and Amazon, alongside pure-play watchlist favorites. Each plays a different role, so grouping them by function helps.

Microsoft monetizes AI through Azure and its Copilot products across Office and Windows. Its OpenAI stake gives it a direct link to frontier model progress.

Alphabet runs Google Cloud and its Gemini model family. Search and advertising still pay the bills, but AI now shapes both.

Amazon sells AI compute and tools through AWS, plus its own model work. AWS remains the largest cloud provider by revenue.

Palantir sells AI decision software to governments and large enterprises. Its commercial US business has grown quickly, and the company has covered this shift across its filings.

ServiceNow embeds AI agents into IT and workflow automation. The company set specific AI monetization targets that it reports against each quarter. I’ve tracked how ServiceNow frames its AI revenue goals and why leadership keeps raising the bar.

Salesforce pushes Agentforce, its AI agent layer inside its customer platform. Adoption numbers are the figure to watch.

Note for publishing: Ticker-level share prices, market caps, and year-to-date returns change daily. Before publish, pull current figures from a named source (Nasdaq, NYSE, or each company’s latest 10-Q/10-K) and add an “as of [date]” line. I have not stated live prices here because I cannot verify them in this session.

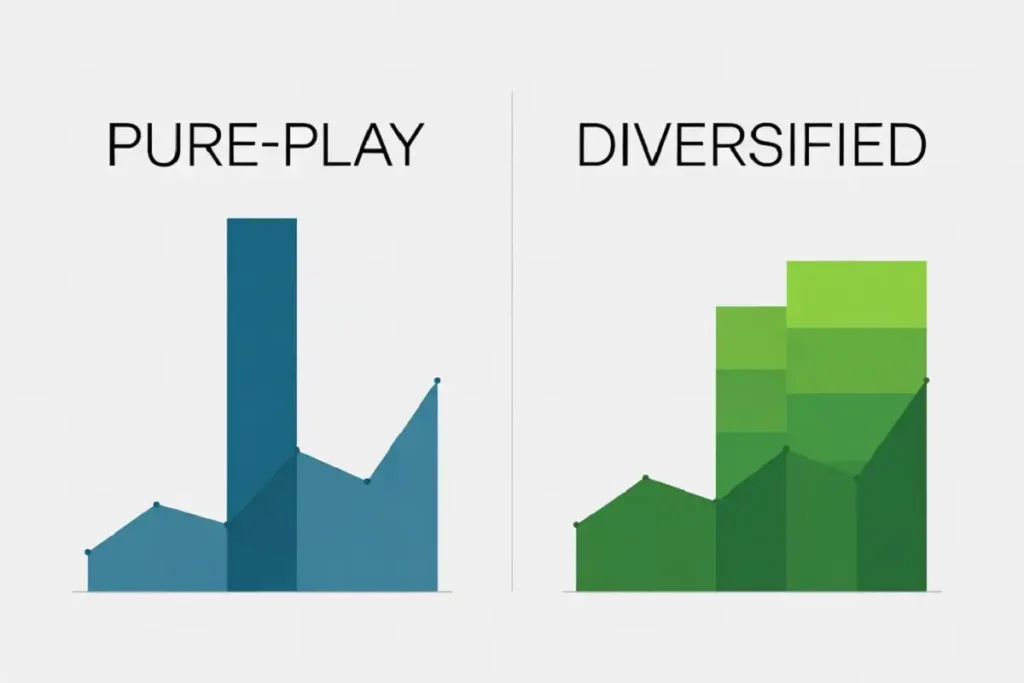

Pure-Play vs Diversified AI Software Stocks

A pure-play AI software stock earns most of its revenue from AI products. A diversified name earns AI revenue on top of a large existing business.

The trade-off is straightforward. Pure-plays give you concentrated exposure and sharper moves in both directions. Palantir is the common example. Diversified giants like Microsoft and Alphabet give you AI upside with a cash-generating base underneath, which softens the swings.

Neither is automatically better. Concentrated bets reward conviction and punish bad timing. Diversified bets dilute the AI story but protect the downside. Your choice depends on how much volatility you can hold.

How to Evaluate an AI Software Stock

Start with revenue growth, then check whether that growth is profitable. AI infrastructure costs are high, so fast revenue with widening losses is a warning sign. Here is the checklist I run before taking any AI software stock seriously.

Recurring revenue. Look for subscription or usage-based income that repeats. One-time deals inflate a single quarter and fade.

Gross margin. Software should carry high gross margins. If AI compute costs crush margins, the model is under strain.

Net revenue retention. This shows whether existing customers spend more over time. A figure above 120% signals real product pull.

Free cash flow. Profitable growth beats growth funded by constant cash burn. Check the cash flow statement, not just the headline.

Valuation multiple. Many AI software stocks trade at high price-to-sales ratios. Ask what growth rate the price already assumes. If the stock needs perfection to justify its price, the risk is priced against you.

Customer concentration. A company leaning on a few large contracts carries hidden risk. One lost client can reset the story.

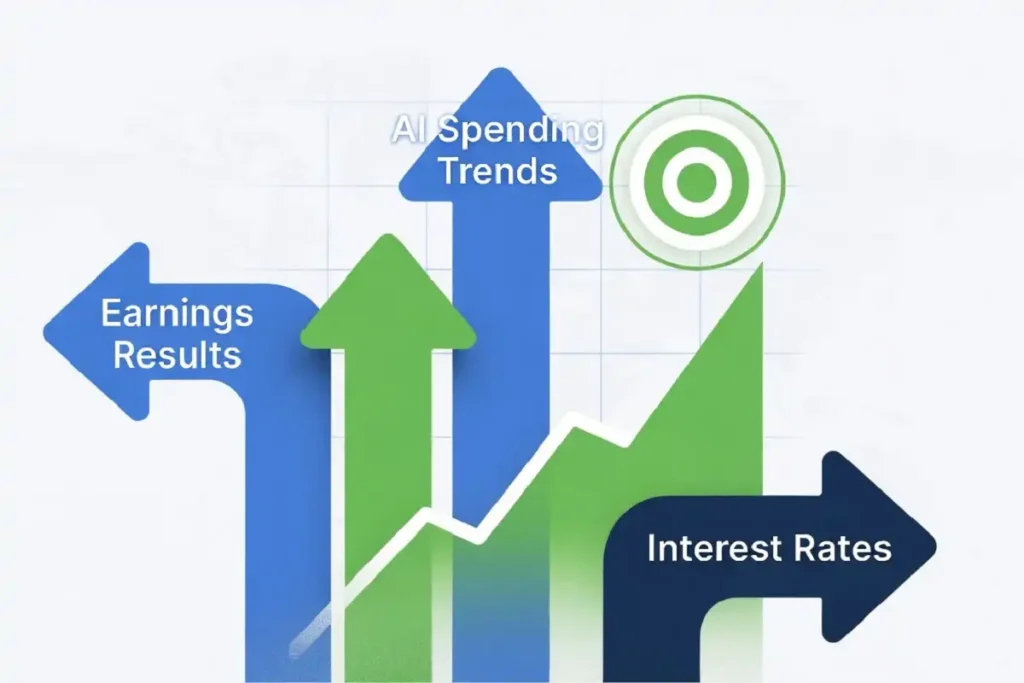

What Drives AI Software Stock Prices?

Three forces move these stocks most: earnings results, AI spending trends, and interest rates. Earnings matter because the market wants proof that AI revenue is real and accelerating.

AI spending trends matter because enterprise budgets set the ceiling for growth. When large companies expand AI budgets, software vendors benefit first.

Interest rates matter because high-growth stocks are sensitive to rate moves. Higher rates pressure richly valued names hardest, since more of their value sits in future earnings. The broader market backdrop feeds directly into these names, and the recent stretch of record index closes shows how quickly AI optimism can lift or drag the whole group.

Are AI Software Stocks in a Bubble?

Some AI software stocks trade at valuations that assume years of flawless execution, which raises real bubble concerns for parts of the group. That does not mean the whole category is overpriced.

The split matters. Companies with durable, profitable AI revenue stand on firmer ground. Names trading purely on narrative, with thin revenue behind the story, carry the most risk. When sentiment turns, the gap between the two shows up fast, and sharp sector pullbacks have already tested how much of the rally rests on fundamentals versus hope.

My read: treat valuation as a risk input, not a reason to avoid the sector entirely. Own quality, size positions sensibly, and expect volatility.

AI Software Stocks vs AI Hardware and Memory Stocks

AI software stocks sell programs and platforms; AI hardware and memory stocks sell the physical layer that runs them. Both benefit from AI growth, but they behave differently.

Hardware and memory names are more cyclical. Their revenue swings with build-out cycles and component pricing. The memory segment in particular moves with supply, demand, and pricing swings that don’t always track software demand. Software revenue tends to be steadier because it recurs monthly or annually. For a fuller picture of that hardware side, the way memory names have traded on AI demand shows how differently the two groups can move in the same market.

Many investors hold both to cover the full AI stack. Software for steadier growth, hardware for cyclical upside.

How to Start Investing in AI Software Stocks

Decide first whether you want individual stocks or a fund, then size your exposure to your risk tolerance. Individual AI software stocks give you control and concentrated upside, but they demand research and a stronger stomach for swings.

Funds and ETFs spread risk across many names. You give up the big single-stock winners, but you avoid betting everything on one company’s execution. For many readers, a blend works: a core ETF position plus a few individual names you understand well.

Whatever route you pick, position sizing protects you. No single AI software stock should be large enough to sink your portfolio if the thesis breaks. Some investors also lean on rules-based approaches, and automated trade signals built around AI have drawn interest from people who want a systematic way in rather than gut calls.

What This Means Going Forward

AI software stocks are no longer a single trade. The category has split into proven revenue engines and speculative bets, and the gap is widening. Focus on recurring revenue, real margins, and valuations you can defend. The figures that matter most next are quarterly AI revenue disclosures and enterprise spending trends, since those tell you whether the growth is holding or fading.