AI Memory Stocks: The 2026 Investor’s Complete Guide

AI memory stocks have become the surprise winners of the artificial intelligence boom. While Nvidia grabbed headlines, the companies making the memory chips inside every AI server quietly delivered some of the market’s biggest gains in 2026. Here’s what’s driving them, and what to watch next.

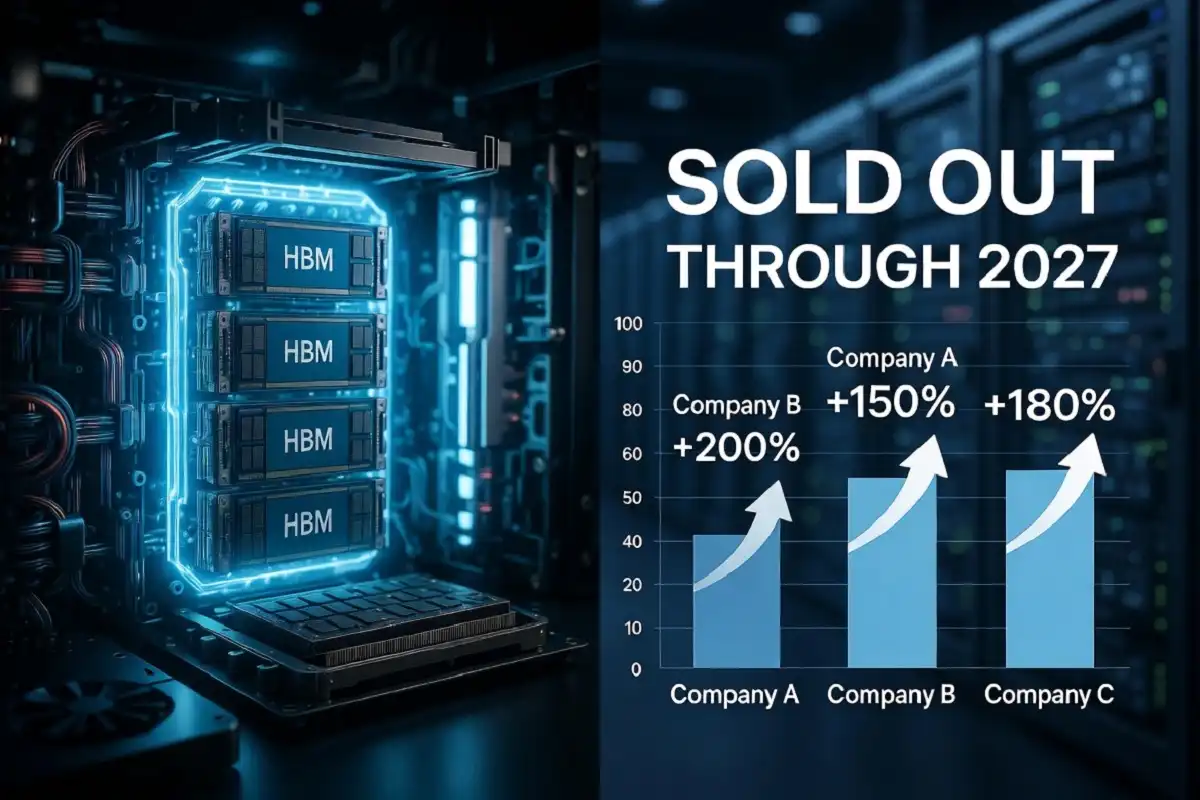

AI memory stocks are shares in companies that make high-bandwidth memory (HBM) and DRAM chips used to train and run AI models. The three leaders are Micron, SK Hynix, and Samsung. All three saw shares surge over 100% in 2026 as HBM demand outpaced supply, with production sold out through 2027.

What Are AI Memory Stocks?

AI memory stocks are shares in chipmakers that supply the specialized memory AI systems need. This is not the regular memory in your laptop. AI accelerators like Nvidia’s GPUs need a specific type called high-bandwidth memory, or HBM.

HBM stacks multiple memory chips vertically and connects them with tiny vertical wires called through-silicon vias. This design moves data far faster than standard memory. AI training and inference workloads are memory-bandwidth-bound, making HBM essential for GPUs like NVIDIA H100/B200 and AMD MI300X.

Put simply, an AI chip is useless without fast memory feeding it data. That makes memory makers a core part of the AI supply chain. When you buy AI memory stocks, you own a piece of that bottleneck.

Three companies dominate the market. The overall DRAM market is largely concentrated among three players, collectively accounting for more than 90% of market share by revenue in 2025, according to IDC. Those three are Micron, SK Hynix, and Samsung.

Why Are AI Memory Stocks Booming in 2026?

AI memory stocks are booming because demand for HBM has exploded while supply stays tight. AI data centers consume massive amounts of memory, and factories cannot build it fast enough.

The numbers tell the story. The memory semiconductor sector is experiencing explosive growth, with industry revenue surging 78% in 2024 to $170 billion. The rally continued through 2026.

Supply is the key. Micron reported record fiscal Q3 2026 results, with revenue reaching $41.46 billion, driven by surging demand for High-Bandwidth Memory (HBM) in AI infrastructure. That revenue more than quadrupled from a year earlier.

Here is the pricing dynamic that matters. Memory manufacturers expect supply-constrained markets through 2026, enabling robust profit margins and favorable pricing conditions across the sector. When supply is tight, makers charge more. Margins expand. Profits jump.

Capacity is fully booked. Micron’s management indicates its capacity is sold out through 2026, 2027, and customers have booked into 2028. New factories will not add meaningful supply for years, so the shortage looks durable.

The Big Three AI Memory Stocks

Micron Technology (MU)

Micron is the only pure-play US-listed option among the top three. Micron has broader exposure to the AI memory stack than Western Digital with HBM, data center DRAM, and NAND, and its 2026 HBM supply is said to be sold out.

The stock’s run has been extraordinary. Micron’s stock price is up roughly 700% over the past year, lifting the company’s market cap past $1 trillion. Yahoo Finance noted that Micron is now the 11th-largest US public company.

Its latest results beat expectations by a wide margin. Revenue came in at $41.46 billion versus $35.84 billion estimated, and the company said it expects revenue of about $50 billion for the current quarter, up from $11.3 billion a year earlier.

The company has locked in future business too. Micron said it has signed 16 long-term agreements with customers such as data center operators and automakers. With HBM capacity sold out through 2027 and $100 billion in contracted multi-year revenue, the company exhibits robust fundamentals.

As of the July 2026 pullback, Micron traded at $984.75, down 22% from post-earnings highs, with an oversold RSI reading of 38.25. That drop reflects profit-taking, not a broken thesis.

SK Hynix

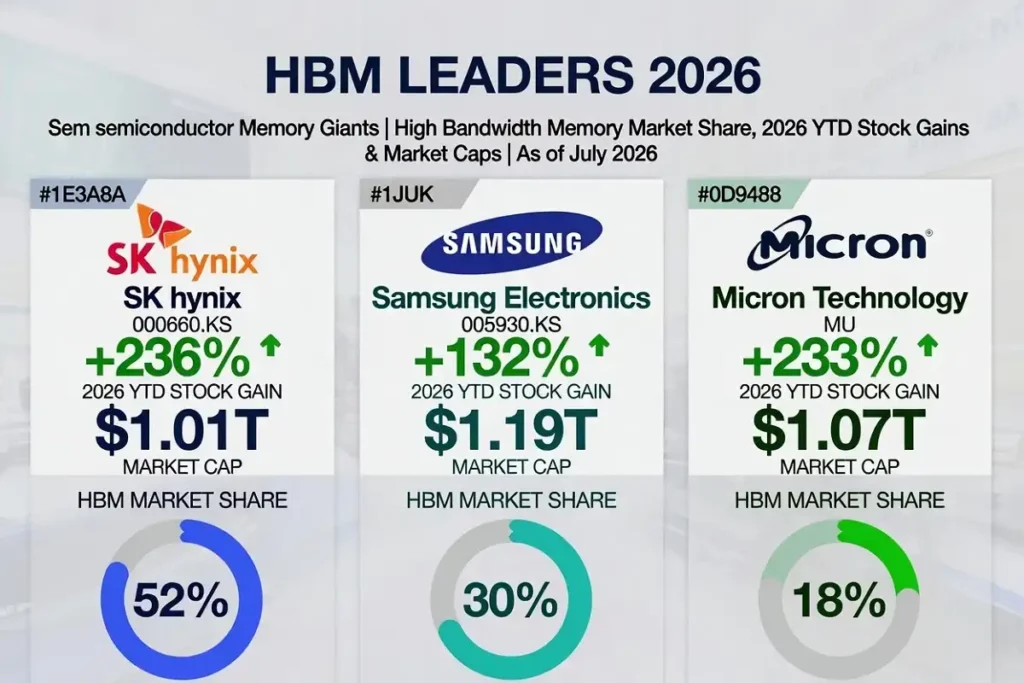

SK Hynix is the HBM market leader and the main supplier to Nvidia. As the first company to mass-produce multiple generations of HBM products, including HBM3 and HBM3E, SK Hynix is a leading player in the HBM market, with a 63.2% market share by revenue in 2025, according to IDC.

The stock has been one of the best performers on any global exchange. Shares in SK Hynix have soared over 280% this year, propelling its market capitalization above $1 trillion.

Its ties to Nvidia run deep. In June 2026, SK Hynix announced a technology partnership with NVIDIA to advance next-generation memory aligned with NVIDIA’s AI infrastructure roadmap.

The most immediate news: SK Hynix is coming to the US market. More on that below.

Samsung Electronics

Samsung is the most diversified memory maker but has trailed rivals in HBM. Samsung holds a stronger position across a more diversified set of memory types. That breadth cuts both ways, since it spreads exposure but dilutes the pure HBM upside.

Samsung shares still rose sharply. Samsung Electronics gained about 165% year to date as of late May 2026.

There is a catch for US investors. Neither SK Hynix nor Samsung is U.S.-listed, which makes them more difficult to access by some investors and for inclusion in indices. That gap is exactly what the next event addresses.

The SK Hynix Nasdaq Listing: A Major 2026 Catalyst

SK Hynix will start trading on the Nasdaq on July 10, 2026, under the ticker SKHY. This gives US investors direct access to the HBM leader for the first time.

The deal is historic in size. The company plans to issue 17.79 million new shares at a value of about $29 billion, expecting to start trading on July 10, though it noted the dates were tentative and subject to change. If priced at the upper limit, it would surpass Alibaba’s 2014 debut to become the largest ADR listing in Wall Street history.

Here is how the structure works. This is an offering of 177.9 million American Depositary Shares, with each ADS representing one-tenth of an ordinary share, at about $158 per ADS. The company already trades in Seoul, so this is an uplisting rather than a first-time IPO.

Demand has been intense. The offering is over seven times oversubscribed, aiming to boost liquidity and index inclusion. Baillie Gifford, Coatue Management, and Situational Awareness Partners, the three cornerstone investors, indicated interest in buying up to $7 billion of the ADS.

Top banks are running the deal. BofA Securities, Citigroup, Goldman Sachs, and J.P. Morgan are the global lead coordinators.

For Micron holders, this listing is worth watching closely. Because SK Hynix is currently the first company to qualify for NVIDIA HBM, this listing provides US investors with exposure to HBM through SKHY rather than Micron, making it the most immediate external factor to watch for MU. Some Micron capital may rotate into SKHY.

HBM4: The Next Growth Driver

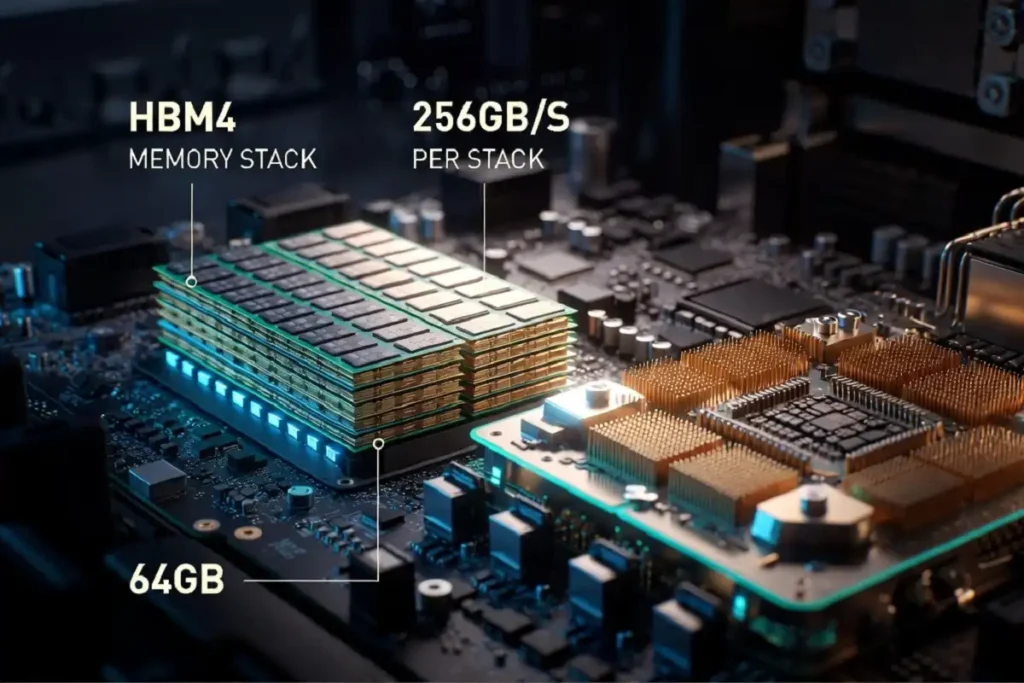

HBM4 is the next generation of AI memory, and all three makers are racing to supply it. This new standard powers Nvidia’s upcoming platform.

The performance jump is real. Micron began volume production of HBM4 with a 36GB, 12-high stack for Nvidia’s Vera Rubin platform, delivering bandwidth above 2.8 TB/s and more than 20% better power efficiency than HBM3E.

Nvidia has certified all three suppliers. On June 5 in Seoul, Jensen Huang confirmed all three HBM suppliers, SK Hynix, Samsung, and Micron, are qualified and actively shipping. That keeps the market competitive while demand stays strong.

The long-term forecast is large. High Bandwidth Memory revenue is projected to reach $100 billion by 2028. HBM4 sits at the center of that projection.

This connects directly to broader AI infrastructure spending. The same forces driving these chips are reshaping corporate strategy, a shift visible in how AI leadership skills now top hiring priorities for executives across major firms.

The Risks Every Investor Should Know

AI memory stocks carry real risks despite their gains. The biggest is the industry’s history of sharp cycles.

Memory has always been boom and bust. Central to the bull run is the belief that the industry has shaken off its past cyclicality, whereby demand fluctuates significantly while supply remains largely fixed. If that belief proves wrong, prices fall fast.

Not everyone buys the “new era” argument. One analyst said he was in Korea advising clients to take profits on parts of their portfolio and rotate into a globally diversified portfolio. Valuations are stretched after such large runs.

Concentration is another concern for Korean exposure. Samsung Electronics and SK Hynix together account for more than 40% of South Korea’s benchmark Kospi, raising concerns that the market could become more exposed to supply chain disruptions and a slowdown in global data center investment.

There are also margin questions. If gross margins peak and capital spending signals future oversupply, investors may return to the old memory-cycle playbook quickly. Watch quarterly guidance for early warning signs.

The SKHY listing itself shows some caution. The debut followed a sudden 25% drop in SK Hynix’s domestic stock price driven by cooling AI sentiment and local regulatory crackdowns on leverage. Sentiment can shift fast.

I’m not a financial advisor, and none of this is a recommendation to buy or sell. These figures are current as of early July 2026 and will change. Do your own research and consider your risk tolerance before investing in any AI memory stocks.

How to Get Exposure to AI Memory Stocks

You have a few ways to invest in AI memory stocks, each with tradeoffs. Your choice depends on how much risk you want and which market you can access.

For US investors wanting a single stock, Micron is the classic choice. For concrete U.S.-listed, large-cap, AI-enabled memory exposure, Micron is the most logical option. It trades on the Nasdaq and sits in major indices.

The SKHY listing adds a second US option starting July 10. That gives direct access to the HBM leader without a foreign brokerage account.

For broader coverage, some investors prefer a basket. A diversified group including Micron, Lam Research, Samsung, SK Hynix, Western Digital, Intel, and Marvell offers complementary exposure to different memory ecosystem segments. This spreads risk across the supply chain.

ETFs are another route. Wedbush managing director Dan Ives added SK Hynix to his IVES exchange-traded fund, saying the company is part of the memory super cycle. A fund removes the need to pick a single winner.

The demand behind all of this ties back to how quickly companies are putting AI to work, a trend covered in our look at the way AI is being adopted across workplaces. More adoption means more data centers, and more data centers mean more memory.

The Numbers to Watch Next

The AI memory story rests on one question: does the supply shortage last? For now, the evidence points to durable demand, with capacity booked through 2027 and HBM4 ramping into Nvidia‘s next platform.

Three things to track from here. First, the SKHY debut on July 10 and how much capital rotates from Micron. Second, whether Micron holds gross margins above 80% into its August quarter. Third, any sign that new factory capacity arrives early and loosens the supply squeeze.

AI memory stocks have delivered rare gains, but they carry the memory industry’s old cyclical risk underneath a new AI story. Watch the guidance, not just the headlines.