Battery Startup Innovation in 2026: Who’s Winning the Race

The battery you’ll charge in five years is being built right now, in pilot lines and pre-A funding rounds. Battery startup innovation moved from lab promise to shipping product this year, and the money is following fast.

Battery startup innovation in 2026 centers on solid-state cells, sodium chemistry, and recycling. QuantumScape, Factorial, and ION are reaching pilot production, while over 120 funded startups share roughly $16 billion in backing worldwide.

What Is Driving Battery Startup Innovation in 2026?

Battery startup innovation in 2026 is driven by one goal: replacing the flammable liquid electrolyte inside today’s lithium-ion cells. Today’s lithium-ion batteries use a liquid electrolyte that is flammable, heavy, and chemically unstable at extreme temperatures. Swap it for a solid, and you get a cell that resists fire, packs more energy, and lasts longer.

That single fix explains most of the current funding. In my reporting on this sector, the pattern is clear. Investors want safety and energy density at the same time. Solid-state chemistry promises both.

The stakes go beyond cars. Longer-lasting cells help power grids, drones, and backup systems. That wider demand is pulling in capital that used to sit only with automakers.

How Much Money Is Flowing Into Battery Startups?

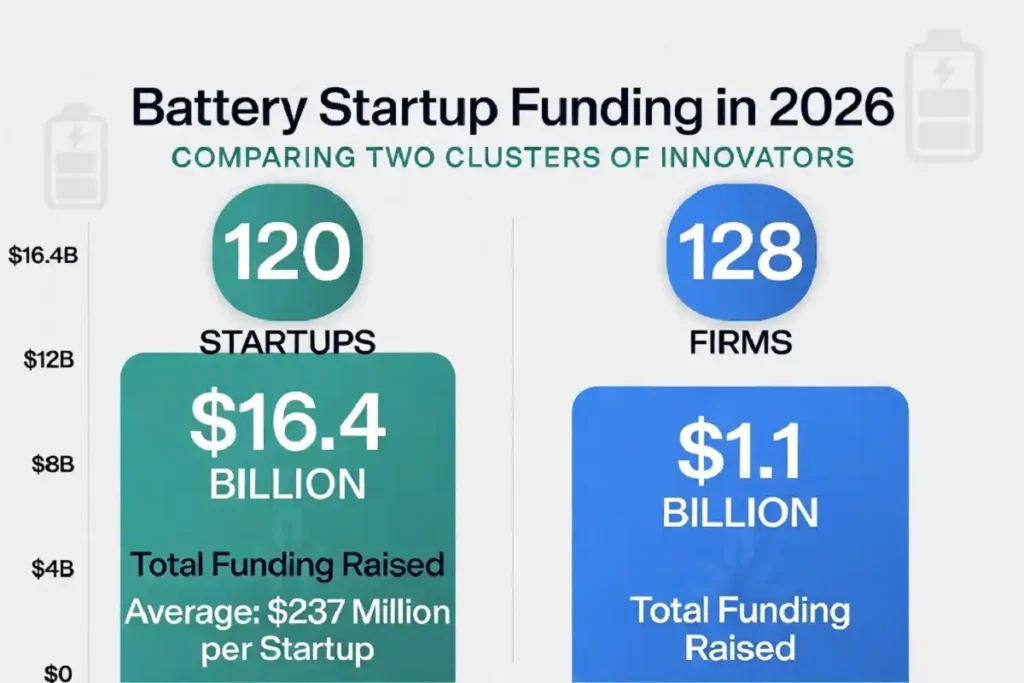

A lot, and it is concentrated. One tracked group of 120 battery startups holds an aggregate funding of $16.4 billion, averaging $237.4 million per company as of May 12, 2026. A separate database counted 128 funded battery companies with $1.1 billion in tracked funding and average funding of $44.8 million as of April 2026.

The gap between those two figures matters. A handful of large players hold most of the money. Many smaller startups run lean on seed and pre-A rounds. This is a top-heavy field, and that shapes who survives.

Capital is also chasing capacity, not just chemistry. In China, the week of January 16 to 22, 2026 saw billions of yuan pour into solid-state capacity plans, even though the technical routes have not yet converged. That mix of heavy spending and unsettled science defines the risk.

Which Battery Startups Lead the Solid-State Race?

QuantumScape leads the US solid-state field on production progress. In Q1 2026, the California company completed installation of its Eagle Line pilot production line and began producing initial volumes of QSE-5 cells. It reported a Q1 net loss of $100.8 million and ended the quarter with $904 million in liquidity. Its QSE-5 cells reached 844 Wh/L energy density and over 1,000 cycles at 95% capacity retention.

The company’s model is capital-light. Volkswagen’s battery unit PowerCo holds a license to produce up to 40 GWh annually, with an option to expand to 80 GWh. QuantumScape supplies the technology. Partners build the factories.

Factorial Energy takes a different path. The Massachusetts startup raised a $200 million round in 2022 led by Mercedes-Benz and Stellantis, then added strategic investment in March 2026 from IQT, a not-for-profit tied to US national security interests. Its semi-solid-state cell claims 375 Wh/kg energy density, well above the 200 to 300 Wh/kg of typical lithium-ion. Factorial is pushing into drones, robotics, and defense, not just cars.

ION Storage Systems shows the smart entry strategy. The Maryland startup brought a solid-state, anodeless battery out of the lab and expects production to begin in 2026, starting with applications where its technology adds immediate value rather than chasing EVs first. That approach mirrors how lithium-ion first entered the market decades ago, beginning with small electronics before scaling to larger uses.

Where Do Chinese Battery Startups Stand?

Chinese startups are hitting production milestones faster than Western peers. Beijing-based Pure Lithium New Energy reached full production on a 500-megawatt-hour all-solid-state line and plans a factory above 1 gigawatt-hour of capacity later in 2026. Its cells achieve between 6,000 and 8,000 cycles, and it closed a Pre-A+ round backed by Yizhuang State Investment.

The giants loom over these startups. CATL holds nearly 40% of the global EV battery market and spent $2.59 billion on R&D in 2024, with a heavy focus on sulfide-based solid electrolytes. A startup competing here faces both scrappy rivals and state-backed champions.

Greater Bay Technology aims for the boldest timeline. Backed by automaker GAC, it targets GWh-scale solid-state production by the end of 2026, using a composite electrolyte blend that hit 260 to 500 Wh/kg in A-sample cells that passed nail and crush tests without fire.

What Chemistries Are Startups Betting On?

There is no single winning chemistry yet, and that is the core risk. Three main solid electrolyte routes run in parallel. Oxides are stable but brittle and crack under repeated cycling. Polymers work only at high temperatures. Halides show promise but are hard to make at scale.

Sodium is the emerging alternative to lithium. CU Boulder spinout Mana Battery is building sodium-based cells, one of several ventures from a university that also produced Solid Power. Sodium uses cheaper, more abundant materials, which sidesteps lithium supply strain.

Recycling forms the third pillar of battery startup innovation. Cylib, founded in 2022, provides sustainable lithium-ion recycling. These startups do not build new cells. They recover the metals that make new cells possible, which strengthens the whole supply chain.

What Are the Real Risks for Battery Startups?

The biggest risk is the gap between lab claims and shipped product. Finnish startup Donut Labs claimed a 400 Wh/kg all-solid-state battery, but faced industry backlash for not providing evidence of its chemistry. That skepticism is healthy. Unverified specs are common in this field.

Cost is the second hurdle. Manufacturing yields stay low and costs stay high, and no one has fully cracked reliable, affordable solid-state production for consumer vehicles. A cell that works in a lab is not a cell you can sell by the million.

Timeline slippage is the third risk. Many startups have promised production dates before and missed them. The startups reaching real pilot lines this year, from QuantumScape to Pure Lithium, are the ones worth tracking. This connects to the broader wave of quantum and AI-heavy deals reshaping how startup funding is allocated in 2026, where hardware bets carry longer horizons than software.

How Startups Fit the Wider Tech Shift

Battery startup innovation sits inside a larger move toward energy-hungry technology. AI data centers, electric drones, and grid storage all need better cells. Factorial’s defense pivot shows how battery makers now court the same buyers driving demand across Bellevue’s defense tech cluster and other security-focused hubs.

For investors, the read is simple. The winners will pair a working chemistry with a realistic manufacturing path. The names with pilot lines running today have the edge. Watch production ramps, not press releases.

The Numbers to Watch Next

Track three figures through the rest of 2026. Watch QuantumScape’s QSE-5 ramp on the Eagle Line and its move to customer field testing with PowerCo. Watch whether Pure Lithium and Greater Bay Technology hit their GWh factory targets on schedule. And watch funding flows, since a top-heavy field means smaller battery startup innovation plays face a tight window to prove out or fold.