Tech Rout: What’s Driving the 2026 Selloff and What Comes Next

The tech rout that hit global markets in June 2026 wiped out over a trillion dollars in value in days. If you hold tech stocks, an index fund, or a 401(k), you felt it. Here’s what triggered the selling, who got hit hardest, and where the smart money is looking now.

The 2026 tech rout was a sharp selloff in technology and chip stocks, driven by AI valuation fears, memory oversupply, and hawkish Fed signals. The Nasdaq 100 fell more than 7% from its June peak. Most losses centered on semiconductors and the Magnificent Seven.

What Is the Tech Rout of 2026?

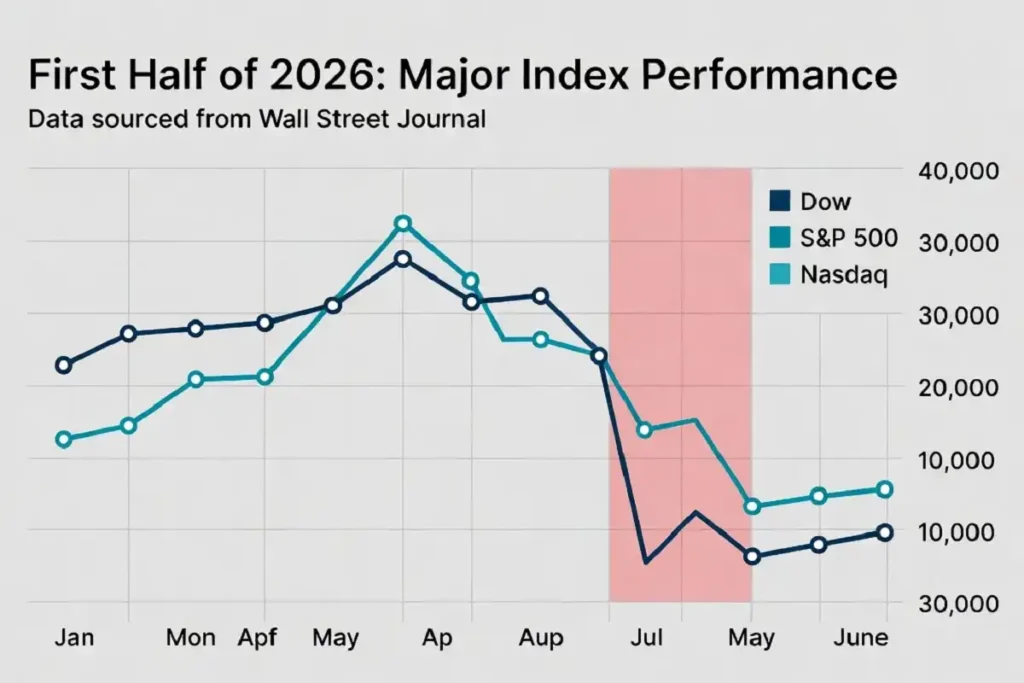

The tech rout of 2026 is a rapid, broad decline in technology stock prices that peaked in June. On June 5, the Nasdaq Composite dropped 4% in a single session. That marked its worst single-day decline since April 2025.

The selling was not random. It hit chipmakers first, then spread to the largest tech names. The Nasdaq 100, which had been riding a nine-week winning streak, suffered a cumulative decline exceeding 7% from its intramonth peak. Hundreds of billions in shareholder wealth vanished fast.

A second wave hit later in the month. On June 23, the Nasdaq 100 fell 3.3%, the S&P 500 dropped 1.4%, and the Philadelphia Semiconductor Index slid nearly 8%. The damage went global overnight.

What Triggered the Tech Rout?

Four forces converged. No single one caused the tech rout, but together they broke the market’s confidence.

First, Broadcom’s guidance spooked investors. Broadcom shares tumbled nearly 15% despite reporting solid quarterly earnings. Management hinted that AI demand growth might slow as customers digest heavy spending. In a market priced for perfection, that hint was enough.

Second, memory chips flashed oversupply warnings. Major memory producers including Micron Technology and Samsung Electronics reported inventory buildups that would likely necessitate production cuts in the second half of 2026. Traditional demand from phones and PCs weakened faster than expected.

Third, the Fed turned hawkish. Hawkish commentary from new Federal Reserve chair Kevin Warsh suggested an interest rate hike could be likely before the end of the year. Higher rates make expensive growth stocks less attractive and raise the cost of the AI buildout.

Fourth, geopolitics added a risk premium. Renewed US-Iran tensions pushed traders toward safety. Tech, with its high-beta profile, took the hardest hit even with little direct Middle East exposure. The parallel pressure on markets echoes the same volatility we covered around the strain on Middle East peace negotiations after US strikes.

Which Stocks Got Hit Hardest in the Tech Rout?

Chipmakers led the losses. The tech rout punished semiconductors before anything else.

On June 23, Nvidia slid 2.8% in premarket trading, followed by Intel down 7.3%, AMD down 7.2%, Broadcom down 3.9%, Tesla down 2.7%, and Alphabet down 1.9%. The pain was not limited to the US.

In South Korea, the Kospi index plunged 10% as shares of Samsung and SK Hynix plummeted more than 12% each. These are the country’s two largest companies by market value.

Memory names fell furthest. Micron and Sandisk tumbled 13% in a single Tuesday session. Marvell Technology, a 2026 standout, gave back gains too. Marvell had posted gains exceeding 300% year-to-date before dropping 8% in one session.

Why Did the Magnificent Seven Fall Together?

The Magnificent Seven fell together because index concentration turned them into a single trade. When selling hit tech, there was nothing else to cushion the blow.

Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla all declined during the pullback, with the group’s concentration in technology and growth factors amplifying the downside. These names drove most of the S&P 500’s gains in 2025 and early 2026.

For passive investors, that concentration became a problem. This concentration risk manifested as portfolio volatility that exceeded historical norms. A handful of stocks moving down dragged the whole index with them.

Is the AI Trade Actually Breaking Down?

No, the AI trade is not breaking down, but the funding model is under real scrutiny. The tech rout exposed a question investors had been ignoring: who pays for all this?

The spending numbers are staggering. Big Five hyperscaler capex is projected at $602 billion in 2026, a 36% increase from 2025, with roughly 75% targeting AI infrastructure. That is more than most countries spend in a year.

The funding source is the worry. Vanguard portfolio manager Thanh Nguyen notes that hyperscaler debt jumped to $93 billion from an average of $28 billion per year. And the borrowing is not done. Nguyen says hyperscalers have only raised about half the funding they need this year.

Analysts have flagged a specific danger: circular funding. Concerns have emerged over funding circularity within the sector and concentration risks as hyperscalers increasingly seek external debt and equity markets to pay for their plans. When companies fund each other’s growth, one pullback can cascade. The broader story connects to how large AI infrastructure deals keep reshaping the sector, where debt and partnerships now drive valuations.

What Does Wall Street Say About the Tech Rout?

Wall Street stayed constructive through the tech rout. Most analysts called it a reset, not a collapse.

Wedbush Securities analyst Dan Ives wrote there was “some added nervousness on the important memory chip trade” ahead of Micron’s earnings, noting the AI trade “remains in the third inning.” His read: this was a gut check, not a top.

Nvidia kept its bullish backing. Nvidia still commanded a Strong Buy consensus rating and an average price target suggesting roughly 40% upside potential from current levels.

Others urged caution on timing. LPL’s Turnquist believes the decline doesn’t imply the tech or AI trade is over, although investors should expect downside volatility as profit-taking pressures come into play.

How Fast Did the Market Recover?

The recovery started within days, but it stayed choppy. Markets did not crash into a bear market. They wobbled, then split.

By late June, buyers stepped back in. On the Wednesday after the June 23 rout, Samsung Electronics rose 10% while SK Hynix added 0.98%, and the Kospi Index climbed more than 3.26%. The panic faded fast.

July opened with mixed signals. Meta surged 11.3% on news it’s building a cloud business to sell excess AI computing capacity, adding $179 billion in market value, while the iShares Semiconductor ETF dropped 4.7% with Micron leading the retreat. Some names soared, others sank the same day.

The first-half scorecard tells the real story. Through June, the Dow gained 8.9%, the S&P 500 rose 9.6%, and the Nasdaq climbed 12.8%, all experiencing painful drawdowns along the way. The tech rout hurt, but the year stayed green.

What Should Investors Watch Next?

Watch three things: chip earnings, hyperscaler debt, and the Fed. Each one can restart or end the tech rout.

Memory pricing is the first signal. Wall Street’s bullish case for Micron depends on HBM4 pricing holding and hyperscaler AI capex not rolling over through 2027. If prices crack, the memory trade breaks first.

The debt load is the second. Morgan Stanley and JP Morgan estimates point to enormous future borrowing to fund the buildout. If credit markets tighten, the AI spending engine stalls.

The Fed is the third. Fed Chair Kevin Warsh said “prices are too high,” which sent Treasury yields higher. Rate hikes raise the cost of everything tech depends on. For readers tracking this, our coverage of how AI skills now shape career and hiring decisions shows the same forces reshaping the job market, not just stock prices.

The Numbers to Watch Next

My read on the tech rout: this was a valuation reset inside a bull market, not the end of the AI story. The fundamentals held. The fear was about price and funding, not broken demand.

The catalysts that sparked the selling are still live. Memory oversupply, hyperscaler debt, and a hawkish Fed have not gone away. Watch chip earnings and any hint that a major hyperscaler is slowing spend. That single headline would matter more than any of the moves we saw in June.