NOW AI Targets: What ServiceNow’s Numbers Say for 2026

Investors are watching one gap closely. ServiceNow trades near $107, but Wall Street’s average target sits far higher. The story behind the NOW AI Targets debate is simple: fear versus fundamentals.

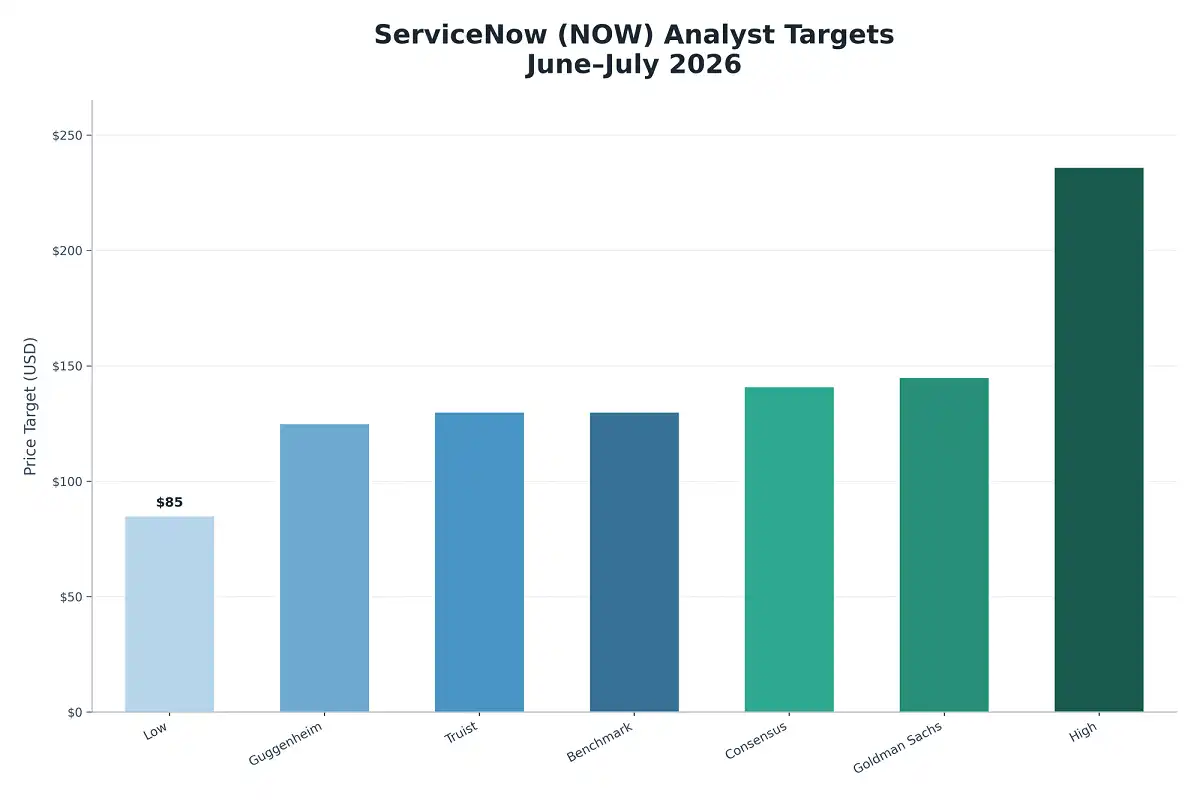

Analysts hold a Strong Buy on ServiceNow (NYSE: NOW). The average 12-month price target sits near $141, with a high of $236 and a low of $85. That implies roughly 35% upside from mid-July 2026 levels.

What Are the Current NOW AI Targets?

The consensus target lands around $141 to $147 depending on the tracker. Across 54 Wall Street analysts, the average price target is $146.91, implying about 37.6% upside from $106.77. Other data sets show tighter figures. A pool of 46 analysts puts the average at $140.95, with 44 buy ratings, 3 holds, and 1 sell.

The spread is wide. That matters. The current NOW AI Targets range shows real disagreement about how fast AI revenue converts. As of July 14, 2026, the stock still carries a “Strong Buy” consensus tag.

Why Is There Such a Big Gap Between Price and Target?

The market priced in AI disruption that has not shown up in results. Shares fell from roughly $207 last summer to $108, even as subscription revenue compounds above 20%. That created an unusual setup for a company that keeps beating guidance.

Here is the core tension. ServiceNow functions as the control layer enterprise AI agents run through. Every OpenAI, Anthropic, and Gemini integration announced this year plugs into its Context Engine and Workflow Data Fabric. Investors feared AI would eat workflow software. So far, the filings point the other way. The NOW AI Targets gap reflects that mispricing debate, and it sits at the center of the broader conversation about which AI software stocks actually monetize their platforms.

How Strong Are ServiceNow’s Fundamentals?

Very strong, based on the latest reported quarter. Q1 2026 subscription revenue hit $3.671 billion, up 19% in constant currency and above the high end of guidance. cRPO grew 21%, operating margin reached 32%, and the renewal rate held at 97%.

Growth is not slowing at the top line. In 2025, ServiceNow’s revenue was $13.28 billion, up 20.88% from the prior year, and earnings rose 22.67% to $1.75 billion. The company also lifted its outlook. It raised FY2026 subscription revenue guidance to a range of $15.735 billion to $15.775 billion.

These numbers explain why so many NOW AI Targets stayed elevated through the selloff.

What Is Driving the AI Story at ServiceNow?

Now Assist is the engine. It is ServiceNow’s generative AI product suite. Now Assist is running so far ahead of plan that management raised its 2026 target from $1 billion to $1.5 billion in a single quarter. That is a rare move.

Adoption is broadening too. Now Assist shows accelerating uptake, with customers generating over $1 million in annual contract value, up more than 130% year-over-year. And bundling is working. Deals attaching three or more Now Assist products grew nearly 70% year over year.

Partnerships add more fuel to the NOW AI Targets thesis. An expanded IBM–ServiceNow AI partnership targets legacy modernization, with first joint offerings expected in the second half of the year. A Hewlett Packard Enterprise tie-up feeds HPE GreenLake data into autonomous AI service delivery on the platform.

Recent Analyst Moves on NOW

Ratings shifted through the spring and summer. Some firms cut targets after Q1. Others upgraded. Here are the confirmed moves I tracked.

Firm actions in June and July 2026:

- Guggenheim’s John DiFucci upgraded the stock on July 2 with a $125 target.

- Truist Securities set a $130 target on July 9, 2026, maintaining a buy rating.

- Benchmark lifted its NOW price target to $130 from $125 and reiterated a Buy rating.

- Goldman Sachs analyst Gabriela Borges lowered the target to $145 from $163 but kept a Buy rating ahead of Q2 results.

The cuts were not about weak results. Recent analyst actions show mixed revisions post-Q1, with cuts from firms like Oppenheimer and Truist, yet consensus remains Buy-oriented, with FY2026 EPS estimates at $4.18. The spread across NOW AI Targets tells you analysts agree on direction but not on pace. This kind of divergence showed up across the sector during the broader software pullback that hit valuations hard.

What Are the Risks to These NOW AI Targets?

AI monetization timing is the biggest one. ServiceNow has still not shown tangible proof of full AI monetization and faces risks in talent retention, early renewals, and pricing pressure. The company must balance heavy investment against margins.

Volatility is another factor. The share price has been more volatile than 75% of American stocks, typically moving about 11% a week over the past three months. Short-term swings are large.

Acquisitions carry risk too. Potential risks include short-term margin pressure from acquisitions like Armis and broader tech spending sensitivity to interest rates. Any weak macro read could pressure the NOW AI Targets further. A single downgrade cycle can move the average fast, as the past three months showed.

When Is the Next Catalyst?

Q2 2026 earnings. That is the date to circle. ServiceNow reports earnings on July 22, 2026, after the market close. The print will test the AI monetization story directly.

Estimates are set. Upcoming Q2 earnings are expected to show around $3.93 billion in revenue, providing visibility into AI monetization progress. A beat likely narrows the gap. A miss likely resets the NOW AI Targets lower. Either way, the report gives the clearest read yet on whether AI is a tailwind or a threat, and it will shape how investors treat NOW against other AI-driven software names for the rest of 2026.

The Numbers to Watch Next

The setup is clear. ServiceNow keeps beating and raising while the stock trades below where most analysts think it belongs. The NOW AI Targets story now hinges on the July 22 earnings print and the pace of Now Assist revenue. Watch cRPO growth, the renewal rate, and whether that $1.5 billion Now Assist figure holds. Those three lines decide if the current NOW AI Targets prove right or too high. My read: the fundamentals justify the optimism, but the timing risk is real, so the wide target range is honest, not lazy.